{kind=link}

This note considers why 60/40 failed in 2022, the structural forces that could make it vulnerable again, and the practical implications for long-term UK savers planning for retirement.

How inflation, correlation breakdowns and leverage exposed the limits of a once-reliable investment rule

For decades, savers have followed a familiar rule: hold a steady 60/40 mix of shares and bonds. The role of high-quality bonds as a ‘hedge’ against potential equity losses has been treated like financial gospel, a recipe for steady growth and built-in safety (chart 1).

Chart 1: Is the classic 60/40 portfolio a golden rule of investing?

Source: Morenti Wealth, 01/01/26

From Vanguard’s LifeStrategy funds, to Legal & General’s Multi-Index funds, to Schroders Managed Balanced products, to Blackrock’s Target Allocation funds, to Colombia Threadneedle’s Universal MAP offering, many popular UK instruments for long-term savers have been built on this foundation.

Markets have a habit of humbling even the most established strategies. In 2022, inflation roared, and both shares and bonds fell in tandem, challenging this old rule of thumb; one didn’t rescue the other.

As we enter 2026, the key question is whether long-term UK savers approaching retirement should rely on this formula, particularly in a world where governments across the developed world appear committed to running large deficits permanently, what economists call ‘fiscal dominance’ (where governments prioritise spending over inflation control).

60/40 Portfolio Performance in Market Crashes: What Retirees Need to Know

Conventional advice, drawing from Modern Portfolio Theory, has been to diversify long-term investments between equities and high-quality debt (the classic ’60/40 portfolio’). These broad asset classes have often shown neutral or even negative correlation in the recent past (correlation measures how two or more investments move together: negative correlation means when one falls, the other tends to rise), providing natural portfolio protection.

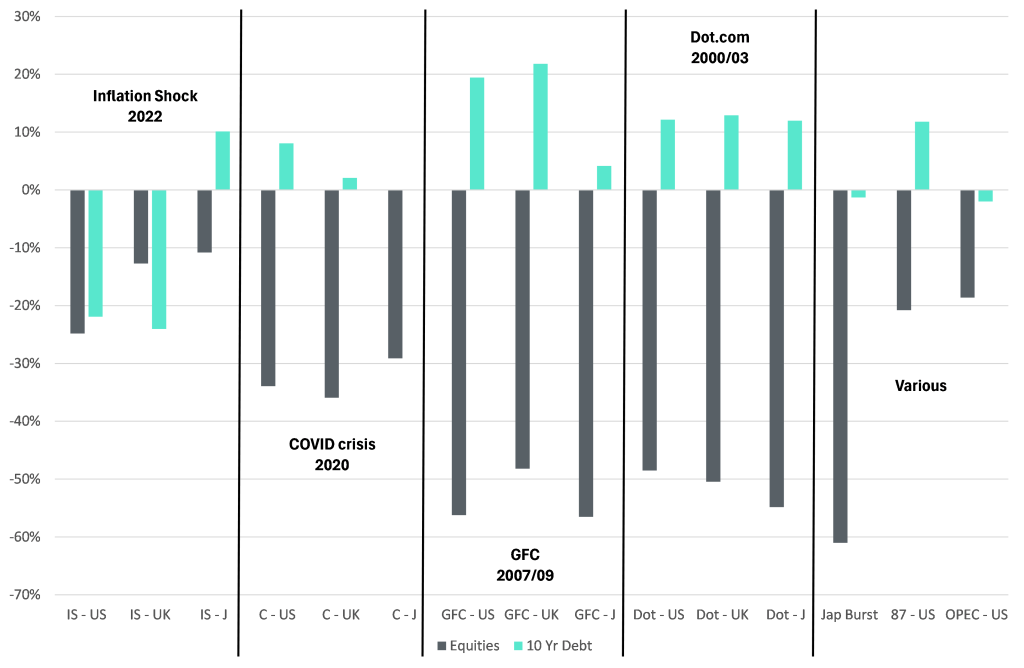

Chart 2 visualises the peak-to-trough price return (the grey bars) of some of the world’s largest equity indices (in the US, UK and Japan) during recent periods of crisis versus the price return provided by 10-year government bonds (debt) in the US (Treasuries), UK (Gilts) and Japan (JGBs).

Chart 2: How key equity indices and high-quality bonds have performed in major crises

Source: Morenti Wealth. We reviewed peak to trough performance for three key equity indices in moments of crisis (1) the inflation shock of 2022, 2) the COVID sell-off in 2020, 3) the Global Financial Crisis (GFC), 4) the dot.com bubble and 5) various, covering the Topix and 10 year JGBs in the early 1990’s following the bursting of the Japanese bubble, the US market in the 1987 crash, and finally, the US market in the original OPEC crisis in 1973 following the Yom Kippur war. For US Equities, we evaluated the return from the S&P500, for UK Equities, the FTSE All-Share and for Japanese Equities, the Topix. For high quality bonds, we used 10-year US Treasuries, UK Gilts and JGBs as proxies. All returns data are in local currency. For clients, further details are available upon request.

Excluding the Inflation Shock (IS) of 2022, higher quality bonds (e.g. government debt) provided a positive return in times of crisis we analysed, whereas equities often collapsed precipitously. This was particularly the case during the Global Financial Crisis (GFC, 2007-2009) and collapse of the Dot.com bubble (2000-2003).

Naturally, market history stretches back further than the 21st century. The 1950’s, 1970’s and 1990’s saw much higher positive correlation between equities and bonds, driven by high inflation. Looking back over several decades, three themes appear to determine whether 60/40 succeeds or fails: the inflation regime, liquidity conditions and policy responses.

Understanding these three factors is crucial for anyone planning their retirement in the next five years, as it helps explain when your portfolio’s natural defences will work and when they might fail.

In deflationary crises, bonds have historically been reliable equity hedges. Central bank rate cuts follow market falls, bond prices rise, and investors flee to safety. This is what happened during the Global Financial Crisis and the Dot.com crash, your bond holdings cushioned the blow from falling shares.

In liquidity shocks, even ‘safe’ assets can sell off temporarily. During the frantic weeks of early 2020, as the COVID-19 pandemic erupted, large institutional funds using borrowed money (leverage) were forced to unwind both stock and bond holdings simultaneously, amplifying the sell-off. Think of it like a crowded theatre where everyone rushes for the exit at once, even the supposedly calm ushers get trampled. By March, US Treasuries had bounced back, though UK Gilts recovered less impressively.

The lesson for your retirement planning: in a severe liquidity crunch, even high-quality bonds may fail to protect your portfolio in the short term, though they typically recover once the panic subsides.

In inflationary shocks, the old rule fails entirely. In 2022, US and UK equities fell sharply, yet at the same time, US Treasuries and UK Gilts also fell. The negative correlation broke down, meaning both parts of your portfolio lost value simultaneously. This development shocked many institutional market participants, let alone individual savers.

In the UK, the situation was exacerbated by large institutional pension schemes (defined benefit plans) that had used borrowed money to buy government bonds as part of their liability management strategies. When bond prices fell sharply, these schemes were forced to sell quickly to meet margin calls, which pushed gilt prices down even further, a vicious cycle that threatened pension security and required Bank of England intervention.

Shares have since rebounded. Bond prices remain well below pre-2022 levels, meaning many savers experienced permanent capital losses in what they thought was the ‘safe’ part of their portfolio.

UK Retirement Planning After 60/40: Protecting Your Pension in 2026

The lesson from 2022 is not that diversification no longer works, but that relying on a single, unchanging formula can leave portfolios exposed when economic regimes shift.

In periods of high inflation or fiscal strain, bonds may not provide the protection they once offered, and the traditional 60/40 mix can behave very different from what many investors expect. This is particularly pertinent today. At Morenti Wealth, we suspect that the COVID pandemic has potentially undermined the classic 60/40 portfolio for good. Why?

Politicians and electorates across much of the developed world appear to desire large government deficits permanently. In autumn-2025 we wrote extensively about the UK’s addiction to government deficits and rising government debt (see ‘Taxes Will Keep Rising…Here’s Why’).

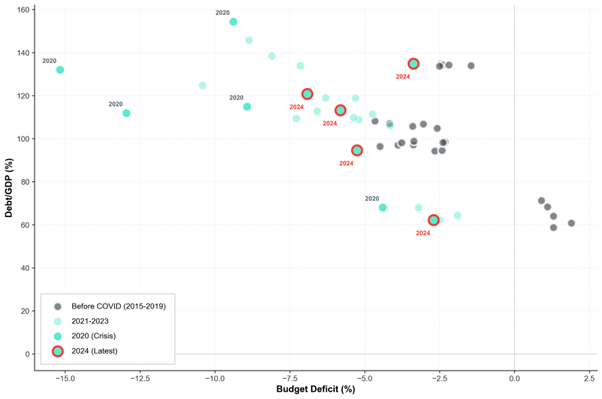

This phenomenon is not isolated to the UK. A similar trend is observable across Europe and the US. Chart 3 shows a scatter plot of annual government deficits since 2015 for France, Germany, Italy, the UK and US (x-axis), plotted against Debt/GDP for each country (y-axis).

Chart 3: A Sample of Government Budget Deficits vs Debt/GDP 2015-2024

Source: Bloomberg, 24/01/2026. Sample includes the UK, Germany, France, Italy and the US.

We have colour coded the data into Before-COVID (2015-2019, charcoal grey) and After-COVID (2020-2024, capri acqua) periods, with the peak of the crisis (2020) and latest available data (2024) clearly identified. For the gimlet-eyed: before COVID, Germany alone ran a budget surplus.

What does this mean for your retirement savings? Large, persistent government deficits tend to get spent inefficiently, creating two key risks: inflation (eroding your purchasing power) and currency weakness (reducing the real value of your savings). In this environment, bond investors may demand higher returns to compensate for increased volatility and inflation uncertainty.

Now, it’s worth noting that government debt has been rising throughout the 21st century, yet during most of this period, bonds and equities showed the beneficial negative correlation we discussed earlier. So why might things be different going forward? The critical difference is the combination of rising debt and the apparent political commitment to maintaining large deficits even during periods of economic growth, what economists call ‘fiscal dominance‘. This creates a persistent inflationary bias (meaning inflation is more likely to run hot than cold) that wasn’t present during the deflationary decades following the Global Financial Crisis.

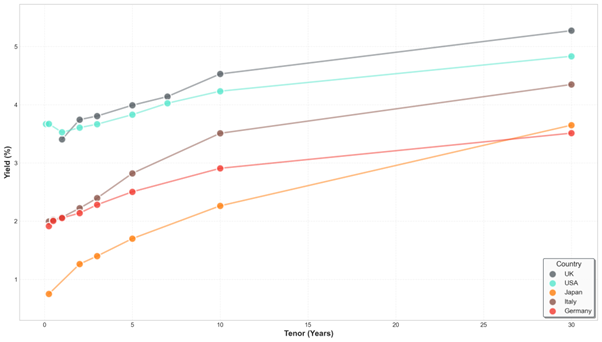

However, context matters significantly. In 2022, bonds entered the inflation shock with historically low yields, offering minimal downside protection and maximum vulnerability to rising interest rates. Today’s higher yields (Chart 4) make high-quality bonds investable again as a form of portfolio insurance, but only in certain scenarios.

When will bonds protect your retirement savings? When growth disappoints, such as during recessions or deflationary shocks, higher-yielding bonds should provide reasonable protection, just as they did during the GFC and Dot.com bust. These are scenarios where central banks cut interest rates, bond prices rise, and investors seek safety.

When might bonds fail you? In supply-side or inflation-driven shocks, potentially triggered by climate-related disruptions, geopolitical energy crises, or other commodity supply constraints, high-quality bonds will likely struggle. Here’s why: in supply-side shocks, inflation rises (due to shortages of key products or resources), while economic growth weakens. This forces central banks, like the Bank of England, to raise interest rates (which hurts bond prices), while at the same time company profits fall (which hurts share prices). The result: both bonds and shares fall together, providing poor insurance precisely when you need it most.

In these latter scenarios, physical assets like commodities and precious metals may prove superior forms of portfolio insurance for your retirement savings. These assets tend to appreciate during supply-driven inflation shocks when both traditional stocks and bonds struggle. Certain emerging market equities with positive exposure to commodity prices, such as resource-rich economies, may provide better diversification than developed market bonds during inflationary episodes.

Chart 4 shows the yield available for a sample of government bonds, covering a wide range of maturities. Whilst these are much higher potential rates of return than available in the recent past (following the near zero interest rate environment post GFC), the actual return from these investments may move much more in line with shares than recent history suggests, meaning they may not protect your portfolio as reliably as they did in the past.

Chart 4: Government bond yields by tenor (remaining time till maturity)

Source: EODHD, 23/01/2026. Yield is the annual interest investors receive as a percentage of the current market price.

Alternative Investments for UK Retirement Portfolios Beyond 60/40

For some investors, introducing a broader range of diversifying assets may improve resilience. The right mix will always depend on individual circumstance, goals and capacity for risk, but understanding the underlying drivers of market behaviour is an important first step.

Commodities and Inflation Protection

As noted above, physical assets like commodities have often moved independently from both equities and fixed income, proving particularly valuable during supply-driven inflation shocks. Research demonstrates that holding a well-balanced mix of commodities can provide inflation hedging as effectively as concentrated positions in any single commodity sector[1].

Gold deserves specific mention. Historically, gold has served dual roles: as an inflation hedge and as a safe-haven asset during periods of geopolitical uncertainty or market stress. While gold’s inflation-hedging properties haven’t been perfect in every period, it struggled during the 1980s and 1990s when inflation fell and real interest rates rose, it has proven valuable across different shock scenarios, particularly when combined with other commodities in a diversified approach.

Alternative Strategies: Proceed with Caution

Alternative strategies can potentially strengthen a portfolio when traditional stock-bond relationships break down, but they come with significant caveats that retirement savers should understand.

Market-neutral strategies, including long-short equity approaches, are designed to generate returns largely independent of equity and bond market movements. During the 2022 inflation shock when both stocks and bonds fell, some well-managed market-neutral strategies delivered positive returns. However, success depends entirely on manager skill, which is exceptionally difficult to identify in advance. For most retirement savers, the challenge of selecting skilled managers, combined with typically high fees, makes these strategies impractical.

Tactical strategies attempt to time markets by shifting allocations based on short-term signals. The evidence here is clear: tactical asset allocation has consistently underperformed simple buy-and-hold strategies after fees, as research from firms like Vanguard has demonstrated.

Macro strategies take positions based on big-picture economic views and can perform well during periods of turbulence. While some macro managers have delivered strong returns during specific periods, the challenge for investors is identifying skilled managers in advance, and even when successful managers are identified, they’re often closed to new capital or require minimums beyond most individuals’ reach.

The ‘Total Portfolio Approach’ is a framework that analyses how all portfolio components interact across different economic scenarios rather than relying solely on historical correlations. While large institutional investors like pension funds have adopted this approach, it requires sophisticated analytics and governance structures that place it beyond the reach of most individual investors. Moreover, there’s legitimate scepticism about whether this represents genuinely new thinking or simply a rebranding of established multi-asset portfolio construction.

The bottom line for retirement savers: Alternative strategies often carry high fees, and realised returns have frequently fallen short of back-tested projections. Performance varies dramatically between managers, and many sophisticated approaches remain impractical for individual investors. If you’re considering these options, professional advice is essential to navigate the complexity and avoid costly mistakes.

Over the coming months, we plan to publish a series of short notes exploring some of the diversification options available to UK savers looking beyond 60/40, including private equity, commodities, precious metals and Bitcoin.

If you’d like to explore how a more resilient portfolio approach could fit your own retirement plan, Morenti Wealth can help you review the options in a clear, evidence-based way.

About Morenti Wealth

Morenti Wealth is a trading style of Burgess & Lee Ltd, an independent financial advice firm specialising in retirement and inheritance tax planning. Morenti Wealth focuses on delivering clear, actionable strategies tailored to clients’ unique goals, stripping away unnecessary complexity and costs. Burgess & Lee is authorised and regulated by the Financial Conduct Authority (FCA).

Disclaimer

This report is for information only and does not constitute personal financial advice. We strive to provide accurate and up-to-date information, but investments carry risks, including the potential loss of capital. This article does not consider your individual circumstances. You should seek personalised advice before making financial decisions.

[1] Ooi, Yao Hua, Thomas Maloney, and Alfie Brixton (2022). “Building a Better Commodities Portfolio.” AQR Capital Management white paper, April 22, 2022